Diversifying retirement portfolios: Why pension fund managers are turning to fine wine

- Pension funds have increased investment in alternative assets like fine wine by 25% over the past two decades.

- Fine wine provides stability and intrinsic value for pension planners, as it is unaffected by geopolitical events or high inflation levels.

- Fine wine has delivered impressive returns of 40.3% over the past five years, making it an ideal asset for retirement planning and diversification.

Change is in the air. As both the bond and equity markets get shaken by turbulence, pension fund managers are increasingly turning to alternative assets, to hedge against economic shocks. According to one report, pension funds around the world have increased their exposure by 25% over the past two decades. The New York Teachers Retirement System, for example, is plunging a whooping 35% of money into alternative investments.

Private equity, property, hedge funds and commodities are among the most enduring alternative assets. However, little by little, institutional investors are dipping into collectibles like fine wine too. One of Canada’s mightiest pension funds, The Public Sector Pension Investment Board, recently acquired 35 iconic vineyards. Goldman Sachs has also been investing heavily in wineries, with a focus on medium and longer-term returns.

In this article, we’ll unveil what’s making wine so appealing to managers today, and how investors could use this unique asset to bolster their own retirement funds.

Fine wine’s intrinsic value is reassuring for pension planners

Unlike most other investments, wine’s world-famous flavors are not impacted by geo-political events or high inflation levels. Instead, they are affected by storage and temperature.

This gives investors – including fund managers – a welcome sense of reassurance. While they may have no control over the stock market, they can ensure that the wine is well cared for.

Over the decades, retirement planners can rest assured that their wealth is not subject to the twists and turns of the stock market. Instead, it comes from the intrinsic value and exquisite quality within the bottle. This can help to mitigate risk and offer valuable diversification.

Investors can find a bottle to match their retirement timeframe

One of the greatest appeals of fine wine is how it improves over time. Naturally, it’s an asset that complements decades-long investment strategies, like retirement plans.

As our CEO, Alex Westgarth, recently commented for Forbes, ‘Fine wine pairs well with younger investors with long-term horizons. A good Bordeaux, for example, can age up to 50 years. This can add a certain stability to your portfolios’.

An excellent wine will always be in high demand as it reaches maturity. And there will almost always be a passionate buyer willing to pay premium prices.

A great advantage for pension planners is that they can probably find a bottle on the market to match their retirement timeframe. While some wines might be best opened in fifty years, others may need just five. Finding the right wine for your unique timeframe can help you to hedge against market losses and meet your investment goals.

With time, premium bottles become rarer

As poet, playwright and novelist, Johann Wolfgang von Goethe famously quipped, ‘Life is too short to drink bad wine’. Ultimately, the asset is made to be enjoyed. People open investment grade wine to celebrate occasions or present as gifts. And, with time, certain vintages will become harder and harder to find.

When demand outstrips supply, prices increase. That’s another reason why long-term investments in wine can be a sensible alternative asset for pension planning.

As the climate crisis continues to impact vineyards, the scarcity factor is likely to further increase prices. The delicate and unique flavors in already-bottled wine could be the last of their kind within just a few years. This will further reduce supply.

Meanwhile, demand is growing by the day. The past decades have seen an impressive rise in Millennial and Gen-Z buyers. Sotheby’s have even noticed the average purveyor’s age shrink from over 60 to under 40.

What’s more, the vast surge of digital advancements are also bringing in new generations and groups of wine buyers.

If demand continues to grow, the tightening supply should lead to a continued increase in value.

Fine wine has an impressive record of beating inflation

There are several reasons why most pension funds begin by investing in equities. It’s partly because managers can afford to take on more risk with longer timeframes. But it’s also to avoid the devastating effects of inflation. Unlike cash, bonds or other debt instruments, equity is generally more inflation-resistant.

Fortunately, fine wine shares this same inflation-resisting quality. This could make it a strong contender for a pension investment plan.

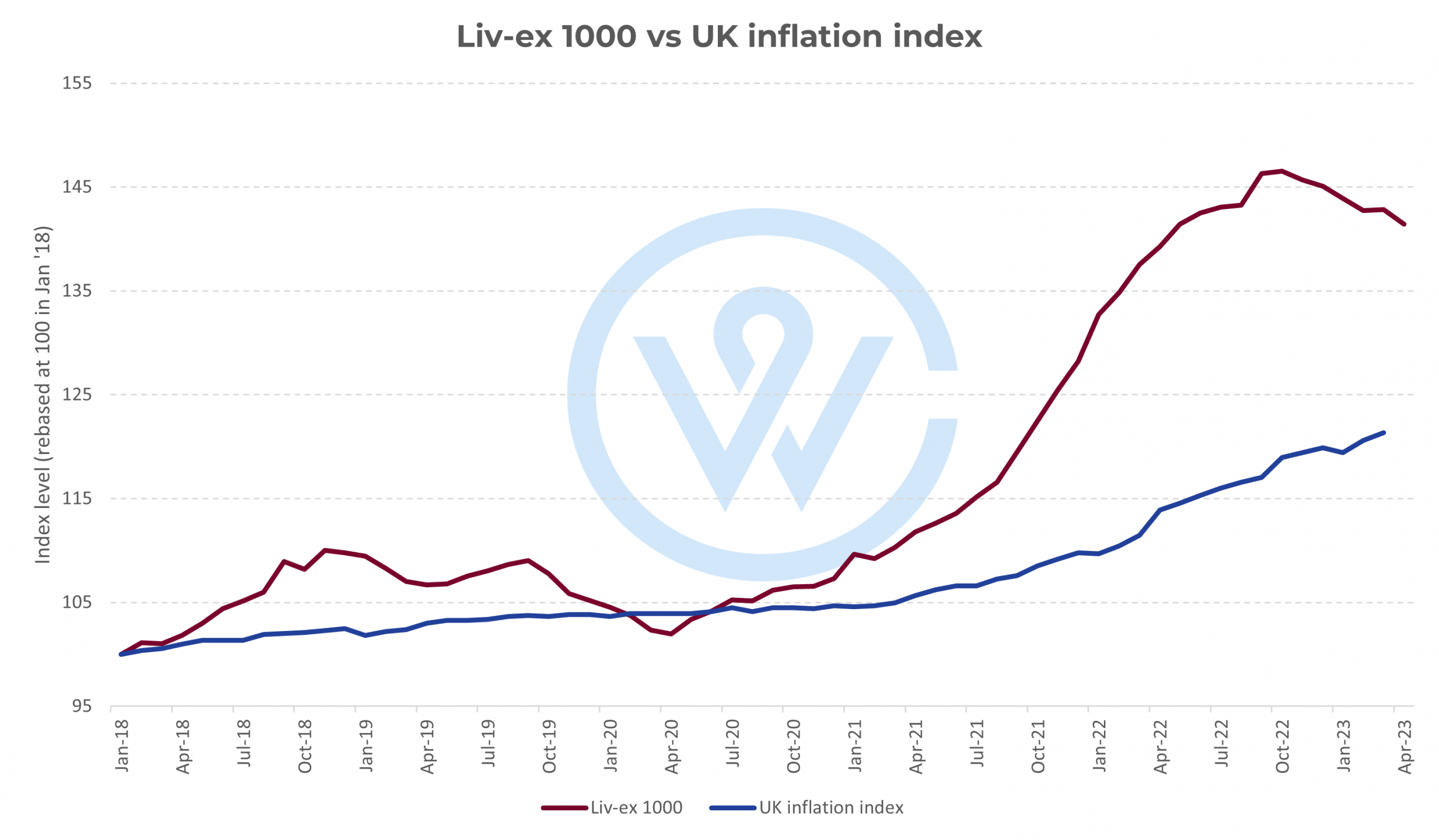

Fine wine has a history of beating inflation. Since 2021, for example, while the UK has endured inflation rates of over 10%, the Liv-ex 1000 index has risen 33%.

During the middle and final investment years – when the pension pot is most at risk of inflation erosion – a healthy allocation to wine could help mitigate the risk.

Fine wine has a history of strong returns

Over the past five years, the fine wine has delivered returns of 40.3%, according to the Liv-ex 1000 index. What’s more, despite the incredibly erratic market, overall performance has been smooth and steady.

This makes fine wine a strong contender retirement planning. Fine wine has both growth and value characteristics, making it well suited for most pension plans.

How can fine wine be incorporated into a pension?

Usually the best way to add wine into private pensions – like workplace and Self-Invested Private Pensions (SIPPs) – is to speak to a financial advisor. This is because they can help you structure the fund in the most tax-efficient way.

When it comes to taxes, fine wine already has a head start. Fine wine is exempt from Capital Gains Tax. Because of this, your advisor may prefer to leave it out of a SIPP altogether and use the tax perks on other assets instead. But probably they would seek to allocate a proportion of fine wine into your overall retirement plan as a hedging asset or long-term growth generator. As an inflation-resistant and illiquid asset, wine generally lends itself to retirement planning well.

If you’d like to find out more about which wines could best suit your pension goals, we’d love to talk to you.